CALL US NOW

CALL US NOWKeeping a Totaled Car: Risks You Should Know

It’s easy to get attached to your car. Whether you’re a collector or a commuter, your vehicle becomes an important part of your daily life. However, when your car is deemed a total loss after an accident, the situation becomes more complex. While the emotional attachment and desire to repair the car may tempt you, it’s crucial to weigh the risks and the long-term consequences. Most body shop owners and insurance experts strongly recommend against keeping a car that has been declared a total loss by the insurance company. If you’re leaning toward keeping your totaled vehicle, here are some important questions to ask yourself first.

What Happens When Your Car Is Totaled?

When your car is totaled, it means that the cost of repairs exceeds the vehicle’s actual cash value (ACV), as determined by your insurance company. Total loss occurs when repair costs or the replacement value of your vehicle surpass the threshold set by your insurer. After this determination, the insurance company will offer you a settlement amount based on your car’s value before the accident, minus your deductible.

While you might think your car is still drivable after a crash, it’s essential to understand the long-term risks, including diminished vehicle value and potential repair complications. You might wonder, can a car be totaled in a rear-end collision? The answer is yes, and if you choose to keep the car, it may be subject to further legal, safety, and financial challenges.

What Is Washington State’s Total Loss Threshold?

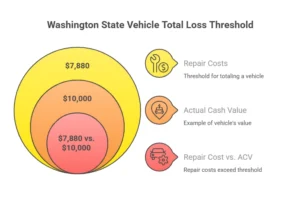

In Washington state, a vehicle is considered totaled if the repair costs exceed the actual cash value (ACV) of the car. The Washington state total loss threshold formula is simple: if the repair costs are more than $7,880, the vehicle is often deemed a total loss. This threshold is used to determine whether your car is worth repairing or if the costs are better served in the settlement payout.

The threshold can vary slightly depending on the make, model, and age of the vehicle, but generally, if the damage exceeds this threshold, the car is considered beyond economical repair. Understanding car accident rates and statistics can provide perspective on how common these total loss determinations are. Understanding this is crucial when deciding whether to accept an insurance payout or try to keep the car.

Can You Drive a Totaled Car?

No, you cannot legally drive a totaled car on public roads in Washington without a transit permit. Once your car is declared totaled, it is typically considered unsafe to drive due to the structural integrity being compromised. You must get a special transit permit from the Department of Licensing if you need to move the car to a repair shop or for inspection.

For vehicles with a salvage title, you can’t legally operate the car unless it has passed inspection and has been rebuilt and re-registered. Driving a totaled car without these precautions can lead to legal consequences and fines, much like Washington states new cell phone laws carry strict penalties for non-compliance.

Can You Even Get a Rebuilt Title?

Washington state requires certain conditions to issue a rebuilt title after a car has been declared totaled. To qualify, the car must meet specific criteria set by the state, including a minimum value threshold of $7,880 before the damage. If the vehicle passes inspection after repairs, you may be eligible to apply for a rebuilt title.

However, getting a rebuilt title comes with significant challenges. You’ll likely need to find a specialty lender if you plan to finance the vehicle, and be prepared for higher interest rates. Additionally, re-insuring a rebuilt car can be costly and complicated, as many insurers will offer limited coverage options.

Do You Owe Money on the Vehicle?

If you have an auto loan on your totaled car, you must check with your lender. Some loan companies may not allow you to keep the vehicle if it’s totaled, or they may require you to pay off the remaining loan balance before you can keep it. Even if the insurer offers a payout, it may not be enough to cover the amount you owe on the loan.

Before making your decision, compare your loan balance with the insurance payout. Knowing what to do after an auto accident is vital for protecting your financial interests. You may end up with little to no financial benefit if the payout doesn’t cover the full loan amount.

What If My Car Is Totaled and I Have No Collision Insurance?

If you don’t have collision insurance, you typically can’t recover damages through your own insurer. However, if another driver is at fault, their liability insurance may cover the damage to your car. This is where Elsner Law Firm can help. If you were hit by an uninsured driver or someone else was responsible for the accident, we can assist in seeking compensation through their insurance or filing a personal injury claim.

Without collision coverage, your options for compensation are more limited, but if you are not at fault, you have the right to seek compensation for your vehicle through the other driver’s liability insurance.

Is It Better to Keep a Totaled Car or Take the Insurance Payout?

Is it better to keep a totaled car or take the insurance payout? The decision depends on your circumstances. If the car has significant damage and will need costly repairs, it may be best to accept the insurance payout and move on. However, if you’re willing to invest time and money into getting the car repaired and re-inspected, keeping the vehicle might make sense for some.

Financial comparison:

-

Repair costs can quickly surpass the vehicle’s worth, especially if the car is given a rebuilt title.

-

Insurance premiums may rise after getting a rebuilt title, and comprehensive or collision coverage may be unavailable.

-

Reselling a car with a rebuilt title can be a challenge as it reduces resale value.

For most people, the insurance settlement is the easier and more financially sound option. If you are unsure, consulting a car accident lawyer in Seattle can help you weigh your options. However, if you have an emotional attachment to the vehicle, weigh the long-term costs carefully.

Can You Insure a Car With a Salvage or Rebuilt Title in Washington?

Yes, you can insure a car with a salvage or rebuilt title in Washington, but it can be challenging. Many insurance companies will not offer comprehensive or collision coverage for cars with these titles. They may only offer liability coverage, and premiums will be higher than for a standard vehicle.

Some insurers might require you to pass a safety inspection before agreeing to cover a salvage or rebuilt car. Additionally, your options for securing coverage with reduced rates may be limited. It’s essential to research insurance providers that specialize in rebuilt title vehicles.

What Can You Do With a Totaled Car? (Alternatives to Keeping It)

If you decide not to keep the totaled car, here are some alternatives:

-

Sell it to a salvage yard – Many salvage yards will offer cash for the parts or scrap value.

-

Donate it – If you’re looking for a tax deduction, donating the car to a charity can be a good option.

-

Sell it privately – If you choose to sell privately, ensure you fully disclose the car’s totaled status to the buyer.

-

Accept the insurance payout – If you don’t want the hassle of repairs or title issues, taking the insurance settlement is often the simplest solution.

If the other party is at fault for the accident, Elsner Law Firm can help ensure you get the best settlement before making any decision. It is helpful to know how to sue someone after a car accident in WA if their negligence led to your total loss.

FAQs

1. What happens when my car is totaled?

When your car is totaled, the insurance company will assess the damage and offer a payout based on the vehicle’s actual cash value (ACV). If the cost to repair the car exceeds its ACV, it will be considered a total loss.

2. Can I drive a totaled car?

No, it is illegal to drive a totaled car on public roads in Washington without a transit permit. Once a car is totaled, it must either be repaired, inspected, and re-registered, or moved using a special permit.

3. Can I insure a car with a rebuilt title?

Yes, you can insure a rebuilt title car, but many insurers will only offer liability insurance. Comprehensive and collision coverage may be unavailable, and premiums tend to be higher.

4. Is it better to keep a totaled car or take the insurance payout?

In most cases, it’s financially better to accept the insurance payout. Keeping a totaled car could lead to higher repair costs, insurance premiums, and difficulty selling the car later with a rebuilt title.

5. What should I do if my car is totaled and I don’t have collision insurance?

If another driver is at fault, their liability insurance may cover the damage. If you have no collision insurance, you should seek medical care immediately following the accident and contact a personal injury lawyer to explore your legal options.

Conclusion

Deciding whether to keep a totaled car or accept the insurance payout can be a difficult decision. While the emotional attachment to your vehicle is understandable, the financial and legal implications of keeping a totaled car often outweigh the benefits. Whether it’s the difficulty in securing rebuilt titles, higher insurance premiums, or the complicated legal procedures, it’s essential to carefully weigh the risks involved. If you’re unsure about your options, especially when another driver is at fault, it’s wise to consult with an experienced personal injury lawyer to ensure you receive the compensation you deserve. Contact Elsner Law Firm at 206-447-1425 for a free consultation and guidance on your next steps.